The Third Letter

Why AI's losses are easy to count, and its gains almost impossible to imagine.

An AI Art company just announced a body scanner. Almost nobody in the AI debate had that on a roadmap. Which says something about the future: it isn’t hard to predict because it’s uncertain. It’s hard because it stays unimaginable until somebody imagines it.

So this week I’m going to ask a machine to imagine the future of our industry. It fails first, in the most instructive way possible. Then I force it to do better. The gap between its two answers is the whole argument.

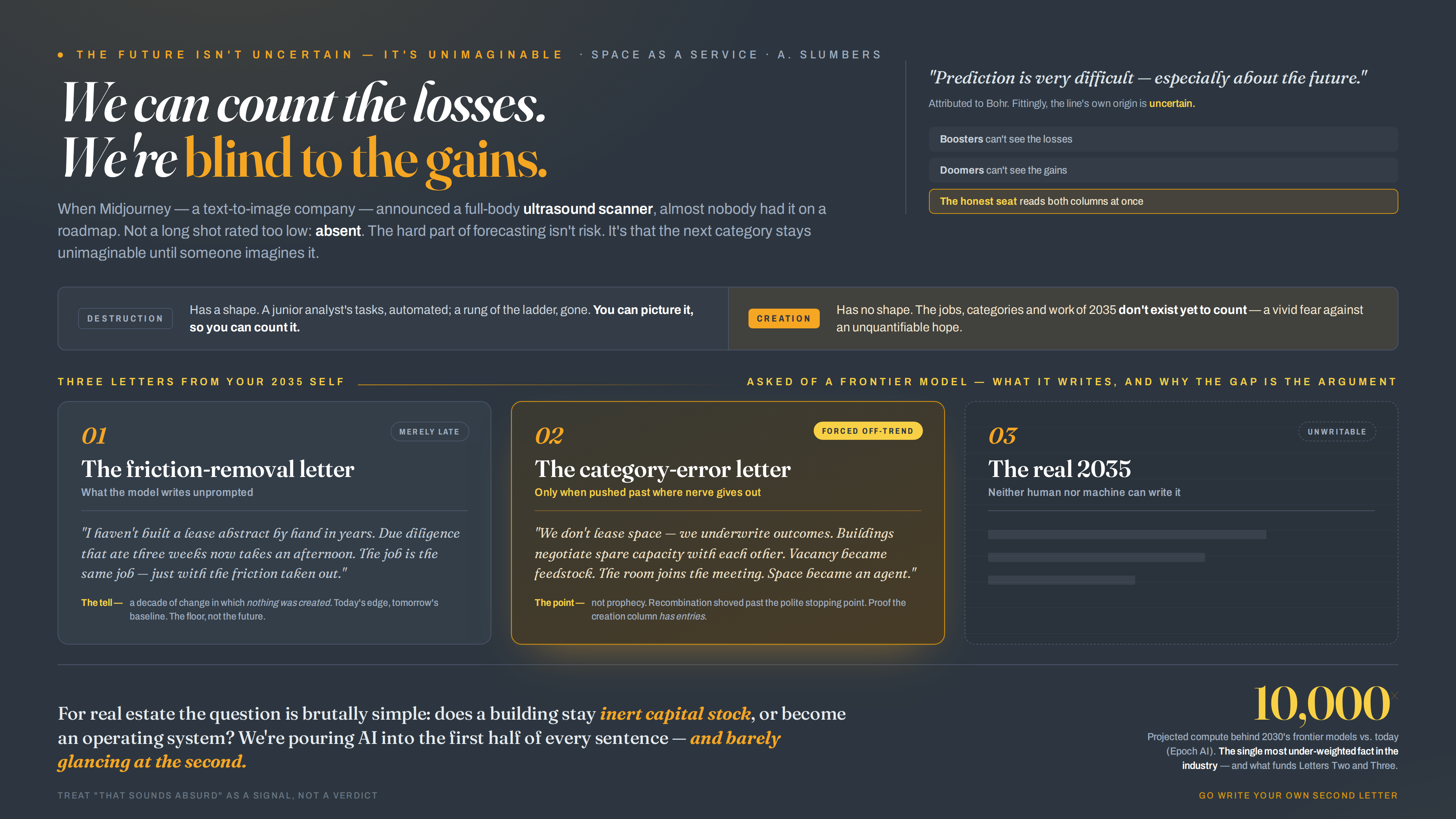

This week Midjourney announced a medical division. Yes, the text-to-image people, the ones who turn ‘a cat in the style of Vermeer’ into a picture. Their first announced hardware project is a full-body ultrasound scanner. You step into a shallow pool, sink through a ring of ultrasound-on-chip sensors, described, wonderfully, as being surrounded by tiny echolocating dolphins, and sixty seconds later walk out with a 3D map of your insides. And they plan to open the first one in a San Francisco spa in 2027. Hot tubs, saunas, cold plunges, and a machine that reads your body.

Put aside whether it works. It isn’t cleared for diagnosis, barely anyone has been through it, and there’s a regulatory mountain between here and a working medical product. None of that is the point. The point is that almost nobody in mainstream AI commentary had this on the map. Not the productivity analysts, not the slide-deck futurists, not most of the people confidently narrating the next decade. An image-generation startup building body-scanning hardware wasn’t a long shot everyone rated too low. It was absent. It sat outside the entire space of things anyone thought to forecast.

WE CAN COUNT THE LOSSES. WE’RE BLIND TO THE GAINS.

The public has soured on AI, and it isn’t stupidity that did it. The destruction is concrete. You can count it. Dario Amodei, founder of Anthropic, makers of Claude, says half of entry-level knowledge jobs could go within five years, and whatever you make of the number, you can picture it: a junior analyst’s tasks, automated; a whole rung of the career ladder, gone. It has a shape.

The creation has no shape. The jobs AI will invent, the categories it will open, the work that pays people’s mortgages in 2035: none of it can be counted, because none of it exists yet to count. So the debate is a rigged fight. A vivid, quantified fear against a vague, unquantifiable hope. Concrete wins every time. Of course sentiment curdled.

And that asymmetry has split the commentary into three camps, only one of which is being honest with you.

The first camp says everything will be fine. These are the tech leaders who spent years insisting AI would change everything, otherwise why pour a trillion a year into it, and who then went quiet on disruption the precise moment the public turned hostile. Now the message has softened to reassurance: new tools, new productivity, nothing to fear, the jobs will sort themselves out. It’s a comfortable story and it is almost certainly false.

The second camp says it’s all catastrophe: mass unemployment, civilisational write-off, the machines win and we lose. Also a story, also too clean, and just as useless because it offers nowhere to stand and nothing to do.

The third camp says something harder, and it’s where I am. Yes, the change is enormous. Yes, much of it will be extraordinary. And no, everything will not be fine. A great deal will change, real people will be really hurt, and amazing things will happen, all at once, and you have to hold all three in your head without letting any one of them cancel the others. That’s the uncomfortable middle. It doesn’t trend on either side of the argument because it doesn’t comfort anyone.

Watch what separates the honest from the rest, because it’s a tell. Amodei kept warning, loudly, after it became unfashionable, precisely so society can prepare: protect the people who’ll be hurt, build the mitigations, lean into the upside with eyes open. There’s a world of difference between predicting destruction to frighten and predicting destruction to mobilise. He’s doing the second. The boosters who fell silent were never doing either, honestly. We must protect the downside as we lean into the upside, and you cannot do the first if you’ve talked yourself into believing there is no downside.

This is not a new pattern, and that’s exactly why I trust it. Ask the handloom weavers of the early nineteenth century. They looked at the power loom and concluded they were finished, and they were right: within a generation a skilled, proud, well-paid trade was gone, and the men who had it died poorer and angrier than they began. The economists looked at the same machine and concluded that employment would recover and the country would grow vastly richer, and they were right too. Both were right. The catch is in the word ‘generation’. The aggregate healed over fifty years; the individual weaver had perhaps fifteen working years left and spent them watching his living evaporate. ‘The system adjusts’ is true and it is the coldest possible comfort to the person whose decade is the one that breaks.

You can run the same tape forward through almost every wave since. The Luddites were not wrong about their own looms; they were wrong only about the long-run aggregate, which is no help at all if you’re inside the short run. By 1950 something like one in thirteen working women in America was a telephone switchboard operator. Automatic switching erased the job almost entirely. The gains were real and the losses were real and they landed on different people at different times, and pretending otherwise is the thing that makes the public stop trusting you.

So hold the two thoughts. Protect people: not as a slogan, as actual policy, retraining, redistribution, a genuine reckoning with who carries the cost. And stay open to a creation side that is every bit as real as the destruction, even though we can’t yet see its face. The boosters can’t see the losses. The doomers can’t see the gains. The honest position is the only one looking at both columns at once.

Which brings me back to Midjourney. The scanner isn’t proof that this particular product will work. It’s proof of something more useful: the creation column has entries we don’t yet know how to name. Nobody could see this one coming, and it arrived anyway, enormous and strange and out of nowhere. That’s the gain side made concrete, for once. The trouble is it only became visible after it existed.

So the question that has been nagging me is whether we can drag the next one into view before it arrives. Can we use these models to help us guess at the third letter? Let me try.

THE MACHINE FAILS FIRST. FLUENTLY.

Prediction is very difficult, especially about the future. Usually attributed to Niels Bohr, though, fittingly for a line about uncertainty, its own origin is uncertain. But our problem runs deeper than prediction. We can’t imagine.

Real estate has its own version of this blindness. Ask people what AI will do to the industry and almost every answer removes friction from today’s work: faster leasing, cleaner data rooms, automated valuation, instant IC papers, predictive maintenance. Useful. Eventually transformative. But still recognisably the same industry doing the same things, quicker. The harder question isn’t what AI subtracts from real estate. It’s what AI lets real estate become.

So I ran the obvious experiment. I asked a frontier model: you’re a CRE professional in 2035, write a letter to your 2026 self about all the amazing things that have happened. Here’s what came back, lightly trimmed:

“Dear 2026 me,

You won’t believe how much easier the work has become. I haven’t built a lease abstract by hand in years: the system reads every document the moment it lands. Due diligence that ate three weeks now takes an afternoon. Buildings basically run themselves, every asset with a digital twin that spots the failing chiller before the tenant feels it. Leasing is faster, pricing adjusts to demand, valuation is real-time. The job is the same job, just with the friction taken out. You’re going to love how much time you get back.”

Read it back and the problem surfaces. Every sentence is plausible. Every sentence is also completely imaginable from where you sit today. There’s nothing in there you couldn’t put on a slide this afternoon. Digital twins, agentic due diligence, dynamic pricing, real-time valuation. It’s the entire efficiency deck, in a warm voice.

And the tell is right there, in the machine’s own words: the job is the same job, just with the friction taken out. It described a decade of change in which nothing was created. Things only got faster. No new category. No new thing a building does. No job that didn’t exist before.

Don’t dismiss it, though. This isn’t the failure. It’s the floor.

Everything in that letter is leading-edge today and will be utterly ordinary by 2035. It’s the homework, not the future. And if you nodded along reading it, look at what you just did. You imagined the subtractive future without breaking a sweat. That’s the trap. The friction-removal story is the easy half of the ledger, and the machine handed it over in elegant prose precisely because it’s the half we can all already see.

NOW FORCE IT OFF THE TREND LINE.

So I changed the rules. Write it again.

Every development has to be one that would have sounded absurd in 2026, the way ‘AI Art company builds a body scanner’ sounds absurd. No efficiency gains. No faster versions of today. Only new categories. Tell me the part of the job that didn’t exist as a job, and the thing my 2026 self would refuse to believe.

“Dear 2026 me,

Stop thinking about your job. It’s the wrong unit. What changed is what a building is*, and therefore what we’re for.*

We don’t really lease space any more. We underwrite outcomes. A logistics tenant doesn’t sign for 200,000 square feet at a rent. They contract for guaranteed throughput, so many units shipped per day at a committed cost, and the building, the robotics, the energy contract and the labour AI are bundled into one number we’re on the hook for. The rent roll isn’t a list of rents. It’s a portfolio of performance guarantees. Half my job is pricing operational risk, which in your day was the tenant’s problem and nobody else’s.

The buildings negotiate with each other. Not as a figure of speech. Every asset runs an agent that knows its own spare capacity, power, cooling, parking, the embodied carbon it has banked, and trades it with the buildings around it. My portfolio sells off-peak cooling to the data centre three blocks over and buys their waste heat in winter. There’s a live market in adjacency. Location stopped being a fixed attribute. It’s a trading position now. We used to call this facilities management. Now it’s a trading desk.

Vacancy stopped being a cost and became a feedstock. An empty floor is raw material. The moment it’s vacant the building reconfigures it into whatever the demand-map says the neighbourhood is short of that month: compute, cold storage, clinical capacity, a film stage, a quiet room people rent by the minute. Space stopped having a use and started having a state that updates. Signing a ten-year lease to fix a use-class for a decade now sounds as strange to me as renting a single web page for ten years would sound to you.

And the one you genuinely couldn’t have pictured: a building carries part of its occupants’ cognition. The space holds the context of the work happening inside it and hands it to whoever walks in. The room joins the meeting instead of just housing it. We don’t sell square footage. We sell a place that thinks alongside you. Turns out that was the product all along. We just couldn’t build it until intelligence got cheap enough to pour into the walls.

You spent years arguing space was becoming a service. You were directionally right, and you under-shot. Space became an agent. Keep imagining. You’re not wrong often enough.”

Now that is a different letter. Every item passes the Midjourney test. Each one would read as a category error today. We don’t lease space, we underwrite outcomes. Buildings running a trading desk for their own externalities. Vacancy as feedstock. The room that thinks alongside you. None of it is a faster version of now. All of it is a different answer to the question of what this industry is even for.

Be clear-eyed about what just happened, though. The machine didn’t conjure this from nothing. It recombined things that already exist, outcome-based contracting, energy trading, carbon markets, agentic AI, and frankly my own #SpaceAsAService thesis, and shoved them past the point where I’d have politely stopped. That’s not prophecy. Most of it won’t happen, or won’t happen like that. Its job was never to be right. Its job was to be imaginable: to prove the creation column has entries, even when we can’t yet read them.

THE THIRD LETTER

So does the trick still work? Yes, but only against resistance. Left alone, the model fails fluently. It hands you the friction-removal letter and you’d have to be paying attention to spot that it told you nothing new. Forced off the trend line, it earns its keep. It won’t predict the future for you. It’ll push your own ideas past where your nerve gives out.

Which leaves me both optimistic and humble. There are really three letters. The first is the future that’s merely late: today’s edge, tomorrow’s baseline. The second is the absurd-sounding one, reachable only when you force the recombination. And the third? The third letter is the real 2035, and neither I nor the machine can write it, because its ingredients don’t exist to recombine yet. Exactly as nobody in 2021 could have written ‘AI art company builds a dolphin spa that scans your body.’

Remember where we’re heading. If current scaling trends hold, the leading models of 2030 could be trained on something like ten thousand times the compute behind today’s frontier. That’s Epoch AI’s central projection, and the International AI Safety Report puts the same growth rate at the same place. Call it a thousandfold and you’re being conservative. Whether it arrives smoothly or in fits and starts, it is my belief that this is the single most under-weighted fact in our industry. The first letter is what that buys when it matures. The second is what it buys once intelligence is cheap enough to live in the walls. The third is everything those two still can’t reach. And there will be a third letter. There always is.

For our industry the question underneath all this is brutally simple. Does a building stay inert capital stock, or does it become an operating system? Does location stay a fixed advantage, or turn into a network position that trades? Does vacancy stay lost income, or become programmable capacity? Right now we are pouring AI into the first half of each of those sentences and barely glancing at the second. The efficiency deck is the first half. The second half is where the industry actually changes.

That’s why I’m optimistic. The losses are real, and we owe it to people to protect them on the way through. The gains are real too, even though their faces haven’t arrived yet. The job was never to forecast. The job is to keep imagining. And to treat ‘that sounds absurd’ as a signal, not a verdict.

So go and write your own second letter this week. Force the machine off the trend line. See what it drags into view. Then remember there’s a third one coming that none of us can write yet.

That’s the one I’m waiting for.